Reduction and Exemption of Income Tax of Foreign Special Professionals

※ Reduction and Exemption of Income Tax of Foreign Special Professionals

-

Who is eligible to apply for the tax incentives for foreign special professionals?

-

A foreign special professional, who has been recognized to have the special expertise announced by the central competent authority, has obtained the foreign special professional employment (work) permit document issued by the Ministry of Labor or by the Ministry of Education, or has obtained the Employment Gold Card issued by the National Immigration Agency, Ministry of the Interior and has met all the following requirements is eligible to apply for the tax incentives.

-

He/she has been approved for the first time to reside in the R.O.C. for work.

-

He/she has engaged in professional work related to the recognized special expertise in the R.O.C.

-

During the last 5 years prior to the day of his/her employment engaged in the professional work or the day of obtaining his/her Employment Gold Card, he/she did not have household registration in the R.O.C. and was not a resident individual of the R.O.C. in accordance with the Income Tax Act.

-

-

A foreign special professional meeting the requirements of tax incentives shall apply for the tax incentives to the competent tax authority when filing his/her annual income tax return in May every year or the departure income tax return before leaving the R.O.C. The required documents are as follows :

-

Application for Exemption from Income Tax for Foreign Special Professionals.

-

A photocopy of the Employment Gold Card with the first-time approval to reside in the R.O.C. for work; in the case a foreign special professional had been previously approved to reside in the R.O.C., the supporting document showing the previous approval not related to the engagement of the professional work is also required (i.e.: a photocopy of ARC for study or as a dependent).

-

An employment contract or another supporting documents showing the employment engaged in professional work is related to the recognized special expertise.

-

-

If a foreigner engages in professional work and meets certain requirements, then within 3 years starting from the tax year in which the foreign special professional for the first time meets the conditions of residing in the R.O.C. for 183 days or more, and having a salary income of more than NT$3,000,000, only the NT$3,000,000 salary income and half of the amount above the NT$3,000,000 in each such tax year shall be included in the gross income for the assessment of individual income tax liability. If the foreigner obtains overseas income set forth in the provisions of Subparagraph 1, Paragraph 1, Article 12 of the Income Basic Tax Act in such tax year, such income shall be excluded from the basic income.

※ For example

Q1.

David, a foreign special professional, has a salary income of NT$8,000,000 related to his special professional work and overseas income of NT$2,000,000 in the applicable year. How does he calculate his income tax relief?

Ans.

1. Amount of non-taxable salary income = (NT$8,000,000 – NT$3,000,000) *50% = NT$2,500,000

Amount of taxable salary income = NT$8,000,000 – NT$2,500,000 = NT$5,500,000

2. Overseas income NT$2,000,000 is excluded from basic income.

Q2.

How do we define the specific point of time for counting the “first 3 years” when a foreign special professional's salary income exceeds NT$3,000,000 and is eligible for the tax incentives?

Ans.

The term "first 3 years" in the tax incentives shall start from the year when the foreign special professional has resided in the R.O.C. for 183 days or more for the first time, and has an annual salary income over NT$3,000,000.

The taxpayer cannot choose the starting year and applicable years as he/she wishes.

Q3.

David, obtaining the foreign special professional employment permit in 2018 and meeting the requirements mentioned in Q3, stays in the R.O.C. for 183 days or more and has an annual salary income over NT$3,000,000 derived from his special professional work in 2018, 2019, and 2020. What is the applicable period of his tax incentives?

Ans.

Year 2018 is the first applicable year and David can apply for the tax incentives from 2018 to 2020.

Q4.

If in the second or third year from the tax incentives applicable year, a foreign special professional does not reside in the R.O.C. for 183 days or his annual salary income does not exceed NT$3,000,000, may the tax incentives be deferred?

Ans.

If a foreign special professional does not reside in the R.O.C. for 183 days or his/her annual salary income is less than NT$3,000,000 within the first three-year period of tax incentives, the tax incentives may be deferred to other employment periods in the R.O.C. for the year when he/she meets the requirements. The total number of years eligible for the tax incentives shall be limited to 3 years, and the deferral period shall start from the first qualified year and continue without interruption for a period not over 5 years.

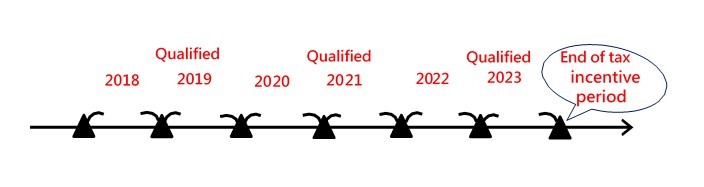

Q5.

David, obtaining the foreign special professional employment permit in 2018 and meeting the requirements mentioned in Reduction and Exemption of Income Tax, stays in the R.O.C. for 183 days or more and has an annual salary income over NT$3,000,000 End of tax Qualified incentive period 2018 Qualified 2019 Qualified 2020 derived from his special professional work in 2019, 2021, and 2023 ( his salary income is less than NT$3,000,000 or the total days of his stay in the R.O.C. are less than 183 days in 2018, 2020 and 2022 ). What is the applicable period of his tax incentives?

Ans.

Since David's salary income is less than NT$3,000,000 or the total days of his stay in the R.O.C. is less than 183 days in 2018, the year 2019 shall be the first qualified year of the tax incentives, year 2019 is the first applicable year. In addition, since David also has salary income less than NT$3,000,000 or the total number of days of his stay in the R.O.C. is less than 183 days in both 2020 and 2022, the tax incentives may be deferred within the following 5 years (from 2019 to 2023). Therefore, the applicable years for David’s tax incentives are 2019, 2021 and 2023.